Why and How PUTTRU has made Africa’s energy transition a priority

‘Making Africa’s energy transition happen: Why and How PUTTRU has made Africa’s energy transition a priority’ is a two-part article.

This first part uses the IEA report on Net Zero by 2050 to set the context. Specifically, to illustrate the sort of ambition needed for a net zero emission future. And, for this reason, why the low level of investment in Africa’s energy sector should be everyone’s concern.

On 18 May 2021, the International Energy Agency (IEA) released its special report on Net Zero by 2050. Since its launch, the IEA report has kicked off a global debate on energy transition. In my opinion, the report has done so with an intensity not experienced before. On the other hand, there has been a growing attention on Africa’s energy transition. And the bulk of these discussions have painted the continent as an unwilling participant in the global energy transition. This is untrue.

This article demonstrates that Africa is a willing participant in the global energy transition and more

Back to the IEA Report…

In brief, the report analyses different scenarios to 2050, including its NZE (net zero emissions) scenario. According to the report, its NZE would enable the world to meet the goal of limiting global temperature to 1.5 degree Celsius above pre-industrial levels[1]. Importantly, the 1.5 degree Celsius limit is required to avert major, future catastrophic impacts of climate change. The report, therefore, calls for an overhaul (largely) of the current energy system. This transformation covers the energy sector itself, transport, industries, and buildings. The strategy is prioritization of renewable energies and technologies that remove CO2 emissions from the atmosphere. Carbon capture, utilization, and storage (CCUS) technology, green hydrogen as well as behavioral changes will feature heavily (IEA, 2021a).

Global warming and what these numbers mean

Basically, the earth’s temperature has grown warmer, and anthropogenic activities (human led actions) have played a significant role. We know this because, due to industrialization, the earth’s temperature is 1.0 degrees Celsius above pre-industrial levels (IPCC, 2018). Furthermore, the IPPC reports with high confidence that at the current pace global temperature will get to 1.5 degrees Celsius between 2030 and 2052 (IPCC, 2018). Indeed, negative impacts on the environment and human welfare is expected at a 1.5 degrees Celsius global temperature. In addition, the situation will be more devastating at 2 degrees Celsius. Thus, the necessity of ensuring that we do not overstep 1.5 degrees Celsius.

Therefore, the big question is: how do we attain high levels of economic growth without further increases in global temperature. Energy economists refer to this as decoupling economic growth from carbon emissions.

NZE scenario & global energy transition leaps

NZE essentially means a huge reduction of emissions. IPCC (2018, p. 13) defines it as “anthropogenic emissions reduced by anthropogenic removals”. For IEA (2021a) Net Zero “means a huge decline in the use of fossil fuels”. And, of course, carbon removal technologies, as captured in the aforementioned IPCC report.

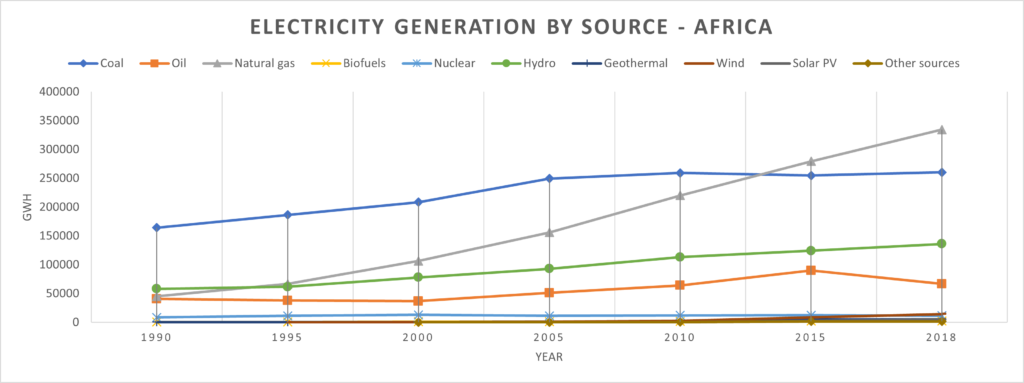

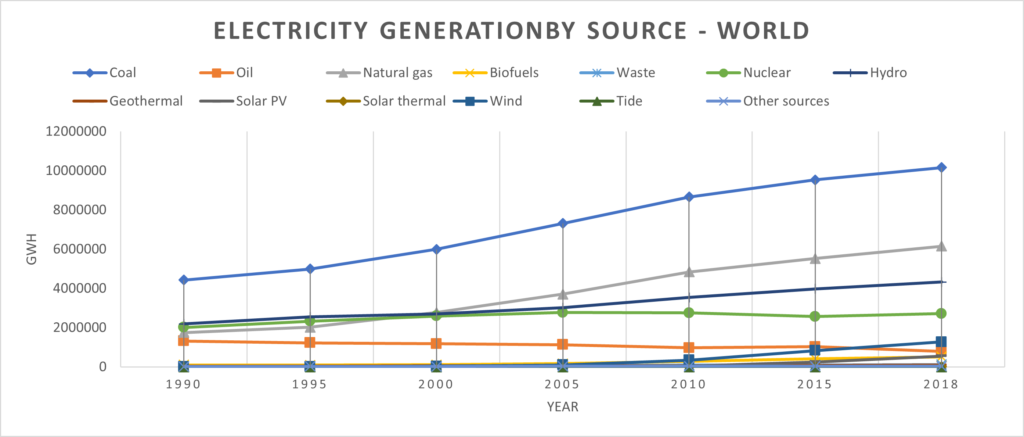

Africa is generating more of its electricity using the cleanest fossil fuel (natural gas). Globally, coal is the No. 1 fuel used for electricity generation.

IEA (2021a) builds on the work done by IPCC (2018) to essentially answer one of the most pressing questions today. The question: what should exist in order to achieve our global energy goals by 2030? This is referring to the UN Sustainable Development Goal (SDG) 7 goal of universal energy access by 2030. Thus, achieving this goal without overshooting 1.5 degrees Celsius.

A pathway, not the pathway, is what the IEA report calls this scenario. The NZE scenario of the IEA report calls for a green electricity take-over. Specifically, the expectation is that 90% of electricity will be generated from renewables. Thus, making green electricity the primary fuel used in sectors like transport and buildings. In the same way, by 2050, all cars worldwide are powered by electricity or fuel cells. This also includes heavy trucks, according to the NZE scenario To illustrate, currently, electric vehicles (EV) account for 4.6% of car sales in 2020. Furthermore, for heavy trucks this is 0.1% in 2020 for fuel cell or EV (IEA, 2021a).

Big changes per sector

Firstly, in the building sector electricity usage should jump from 33% in 2020 to 66% in 2050. Specifically, buildings, globally, should use the most efficient appliances on the market from 2035, according to IEA (2021a) report. Secondly, for industries, the big changes will come from CCUS, hydrogen and electrolyser (for generating green hydrogen at industrial sites). Importantly, for fossil fuels, NZE requires that no new oil and gas fields are developed. This goes for coal mines as well. For both cases, except those already approved in 2021. Hence, this green electricity take-over would require, amongst others, significant installation of solar PV. For example, this should be “equivalent to installing the world’s current largest solar park roughly every day” (IEA, 2021a; p. 14).

Where is Africa in all these?

Similarly, developing and emerging economies are expected to take part in these NZE big jumps. Just as advanced economies, African economies are expected to go green in sectors covering energy, transport, industrial and building. Thus, these economies are to adopt the use of the most energy efficient appliances in buildings. In addition to that, EV or fuel cell powered vehicles and installation of carbon removal technologies in industries. Moreover, African countries are expected to introduce carbon prices starting from 2025 as shown in the table below:

Table: CO2 prices for electricity, industry, and energy production

| USD(2019) per tonne of CO2 | 2025 | 2030 | 2040 | 2050 |

|---|---|---|---|---|

| Advanced economies | 75 | 130 | 205 | 250 |

| Selected emerging market and developing economies* | 45 | 90 | 160 | 200 |

| Other emerging market and developing economies | 3 | 15 | 35 | 55 |

Indeed, such big-jumps initiatives are great opportunities for Africa. Especially given that the continent has already made significant leaps towards a low-carbon economy.

Decarbonization of Africa’s power sector

For instance, according to IEA’s data[2], the continent as a whole, is generating more of its electricity using the cleanest fossil fuel (IEA, 2021b). Whereas, globally, coal is the No. 1 fuel used for electricity generation (IEA, 2021b).

Renewable energy installations are perceived to be more expensive, upfront. However, this has not held African countries from adopting them. At the regional level and/or country levels, African countries have committed themselves to meeting the SDG 7 goals. Consequently, some of these countries have developed (and tested at some scale) institutional reform instruments on feed-in tariff, net-metering, and others to promote renewable energy[3]. Moreover, this is similar to what has been used in European countries to increase renewable energy uptakes.

Examples from the Continent

The Economic Community of West Africa (ECOWAS) is a good example of a widespread political support for sustainable energy. Examples include, the ECOWAS Renewable Energy Policy and ECOWAS Energy Efficiency Policies. Another is the ECOWAS Policy for Gender Mainstreaming in Energy Access. These policies were adopted by the ECOWAS heads of state and, thus, demonstrates a high level of political support. Furthermore, on 3 June 2021, led by the African Union Commission (AUC), Africa launched the AfSEM – Africa Single Electricity Market. AfSEM is expected to play a key role in achieving universal energy access in Africa. Furthermore, the market will be instrumental in decarbonizing the electricity sector (AUC, 2021).

These are only a few examples from the continent.

It is time to recognize Africa as a frontrunner in the energy transition

On one hand, the continent, may be facing an energy supply and energy security challenge. Nevertheless, countries are not just pursuing energy access, but access that is in tune with the global energy transition.

Unfortunately, more attention is given to the energy poverty challenge in the region. This attention should rather focus on the fact that the continent has a cleaner electricity sector. Furthermore, that bold policy innovations are taking place, despite the low level of investment flowing into Africa’s energy sector.

Many of the policy innovations in the continent have happened through North- South collaborations

Concluding Part 1

In conclusion, there is no question of Africa’s readiness for an NZE future. This may not look like the NZE in the IEA report (which rightly notes that its NZE is a pathway, not the pathway).

Nevertheless, the real question is how much the rest of the world is ready for a global net zero emission? For instance, annual investment in electricity generation should increase to USD 1.6 trillion in 2030 (IEA 2021, p.153).As we know, SSA is the region where most people do not have electricity. Therefore, this is where the larger part of investment for new infrastructure to meet a global NZE should go. North- South collaborations, particularly by investing in Africa’s energy sector, will make a global NZE future possible.

In the next article we will be covering a little more on where the opportunities lie for investment in Africa. Furthermore, how we at PUTTRU are doing our bit to make Africa the catalyst for a global NZE.

[1] See IPCC (2018) special report on Global Warming of 1.5 °C available at: SR15_SPM_version_report_LR.pdf (ipcc.ch)

[2] See Data Tools at: https://www.iea.org/data-and-statistics/data-browser?country=WEOAFRICA&fuel=Electricity%20and%20heat&indicator=ElecGenByFuel

[3] See Ghana Renewable Energy Act (2011), Requirements for electricity generation; See EU (2016) for Cabo Verde, Policy for net metering and PURA (2012): The Gambia: New Renewable Energy Law and Feed-in Tariff Rules and UNIDO (2013): Feed-in Tariff Model and Standard PPA.

Reference List

IEA (2021a). Net Zero by 2050: A Roadmap for the Global Energy Sector. Available at: https://www.iea.org/reports/net-zero-by-2050

IEA (2021b). Data tools: Available at: https://www.iea.org/data-and-statistics/

IEA (2021c). The Global Commission on People-Centred Clean Energy Transitions. Available at: https://www.iea.org/programmes/our-inclusive-energy-future

IPCC (2018). Special Report on Global Warming of 1.5 °C: A Summary for Policymakers. Available at: https://www.ipcc.ch/site/assets/uploads/sites/2/2019/05/SR15_SPM_version_report_LR.pdf

AUC (2021). Concept Note: launching of the African single electricity market (AfSEM). Download here.

Ghana (2011). Ghana Renewable Energy Act. Available at: http://www.energycom.gov.gh/files/RENEWABLE%20ENERGY%20ACT%202011%20(ACT%20832).pdf

EU (2016): Download here.

PURA (2012): The Gambia: New Renewable Energy Law and Feed-in Tariff Rules. Available at: https://pubs.naruc.org/pub.cfm?id=538EDD50-2354-D714-5157-A96AE93846C1

UNIDO (2013): Feed-in Tariff Model and Standard PPA. Available at: https://open.unido.org/api/documents/4743695/download/FEED-IN%20TARIFF%20MODEL%20AND%20STANDARD%20PPA